By Steven Ehrlich, Maria Gracia Santillana Linares, Nina Bambysheva| Apr 26, 2024

With bitcoin soaring once again, blockchains are suddenly much more valuable. More than 50 of them are now worth over $1 billion—despite many having few users

[CAPTION]A Forbes investigation reveals that even though only a handful of blockchains other than Bitcoin and Ethereum have gained significant traction, there are no fewer than 50 blockchains today trading at values of more than $1 billion, of which at least 20 are functional zombies.

Illustartion: Nicolas Ortega for Forbes India[/CAPTION]

[CAPTION]A Forbes investigation reveals that even though only a handful of blockchains other than Bitcoin and Ethereum have gained significant traction, there are no fewer than 50 blockchains today trading at values of more than $1 billion, of which at least 20 are functional zombies.

Illustartion: Nicolas Ortega for Forbes India[/CAPTION]

In 2O12 when blockchain pioneers Jed McCaleb, Arthur Britto and David Schwartz created Ripple Labs and its new cryptocurrency, known as XRP, they envisioned a new global financial standard that would enable banks to transfer money rapidly with minimal fees. During its first decade, dozens of financial institutions, including Bank of America and Banco Santander, signed up, eager to test Ripple’s new network. To fund their ambitious project, executives at the company created 100 billion XRP tokens and sold $1.4 billion worth to the public. In early 2018, at the height of the first wave of crypto euphoria, XRP was trading with a market value of $132 billion, giving co-founder and executive chairman Chris Larsen a net worth of $8 billion.

_RSS_In terms of global money flows, not much is going on at Ripple Labs today, and few expect it ever to disrupt the Belgian banking cooperative known as SWIFT, which facilitates $5 trillion in interbank transfers every day. Despite failing at its primary mission, Ripple’s blockchain, a ledger of XRP transactions, continues to hum along. It’s largely useless, but the XRP token still sports a market value of $36 billion, making it the sixth-most valuable cryptocurrency. Larsen remains a billionaire, worth an estimated $3.2 billion. Last year, Ripple’s XRP ledger earned a mere $583,000 in fees processing transactions across its network, according to Messari. In Wall Street parlance, that would give XRP a “price-to-sales” ratio of 61,689. Nvidia, the market’s hottest stock, with a market capitalisation above $2 trillion and revenue of $61 billion, has a price-to-sales ratio of 37.

Ripple Labs is a crypto zombie. Its XRP tokens continue to trade actively, some $2 billion worth per day, but to no purpose other than speculation. Not only is SWIFT still going strong, but there are now better ways to send payments internationally via blockchains, especially stablecoins like tether, which is pegged to the US dollar and has $100 billion in circulation.

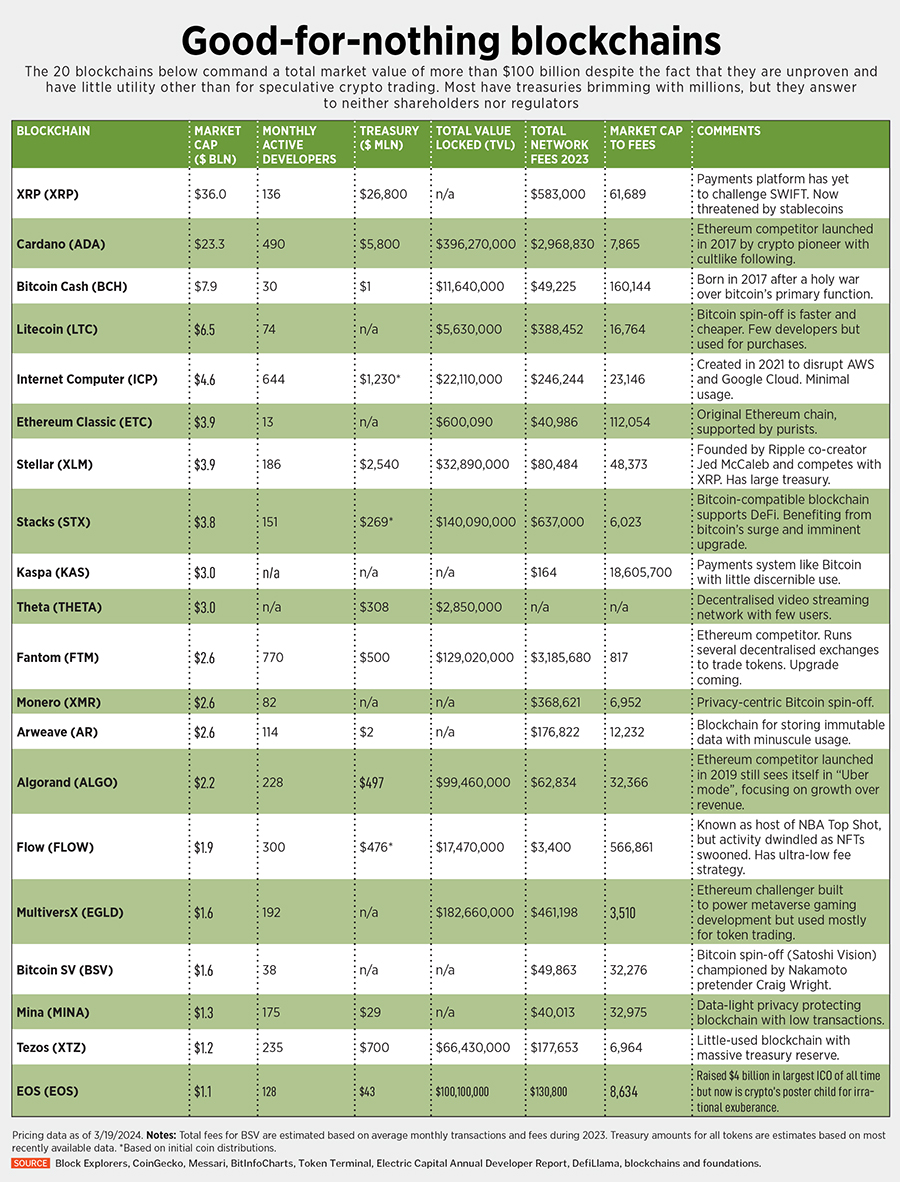

Ripple is not alone. A Forbes investigation reveals that even though only a handful of blockchains other than Bitcoin and Ethereum have gained significant traction, there are no fewer than 50 blockchains today trading at values of more than $1 billion, of which at least 20 are functional zombies. In the wake of the SEC’s approval of spot bitcoin ETFs, crypto markets are soaring. The 20 blockchains Forbes analysed (see ‘Good-for-Nothing Blockchains’), whose quixotic ambitions range from a universal world computer to an untraceable payments network, have a combined market value of $116 billion. Most have few users.

But don’t expect XRP or any of these crypto creations to shutter operations anytime soon. With billions sitting in their coffers, Ripple and others can continue to exist for years. Ripple currently has $24 billion worth of XRP tokens in escrow that it can sell over the next four years.

Currently, the San Francisco company has 900 employees and continues to issue press releases for things like its recent acquisition of digital asset custody operation Standard Custody & Trust. After more than a decade in existence, it is still running pilot crypto programs with central banks in places like the nation of Georgia and the South Pacific Republic of Palau.

“It’s like early-stage venture capital funds or companies that raise too much money and don’t know how to adequately deploy it,” says Matt Hougan, CIO of Bitwise Asset Management. “There’s no way to return the treasury to the investors.”

Moreover, in the bizarro world of digital assets, rich zombie blockchains need not worry about the kinds of things that keep traditional companies on their toes. There are no shareholders or regulators asking for financial statements, and short selling tokens is relatively difficult. So long as there is an ample supply of speculators willing to trade the tokens, flush zombie blockchains will continue to roam the digital landscape.

Says one venture capitalist who requested anonymity, “There’s no wind-down process for a dead crypto protocol.”

Zombie blockchains mostly fall into two categories: They are either spin-offs of earlier blockchains like Bitcoin and Ethereum or direct competitors to them. Spin-off (aka “hard fork”) zombies include Bitcoin Cash, Litecoin, Monero, Bitcoin SV and Ethereum Classic. These five blockchains collectively trade at a valuation of $23 billion today. They are largely the result of disagreements between programmers over how Bitcoin or Ethereum should be run. Because the code underlying these blockchains is open source, anyone can repurpose it for any reason. When the coders can’t get along, a group of them will split off and create a new network, a schism known as a hard fork. Each time a new chain is created this way, it shares the same history as the original chain. And like stock spin-offs, this means that all token holders at the time of the fork receive the same number of tokens on the new chain that they own on the original.

Litecoin was an early Bitcoin fork. It launched in 2011 as a faster, cheaper version for sending payments. It produces blocks four times faster than Bitcoin, an average of one every 2.5 minutes against every 10 minutes for Bitcoin. Like Bitcoin, it processes transactions via proof of work, meaning lots of computers are spinning their wheels (and burning electricity) solving pointless mathematical equations. Also like Bitcoin, it has a hard limit on its token supply, 84 million versus Bitcoin’s 21 million. Today Litecoin has a market capitalisation of $6.5 billion, but last year it booked just $389,000 in fees, compared to $800 million for Bitcoin. Blockchain users pay fees to miners as an incentive for them to process their transactions in the next block they create. The fees generated by zombie blockchains like Litecoin are minimal, indicating a lack of demand for the platform. These blockchains also have trouble attracting developers. As of the end of 2023 there were only 74 monthly active open-source developers supporting Litecoin, according to Electric Capital’s Developer Report, compared to more than 1,000 for Bitcoin and 7,000-plus for Ethereum.

Also read: Can the Bitcoin revival reshape the future of finance?

Bitcoin Cash is worth even more than Litecoin, with a market cap of $7.9 billion, yet it has only 30 monthly active developers supporting it and $49,000 in 2023 fee revenue. Bitcoin Cash was born after an acrimonious split with Bitcoin in 2017 over whether to increase Bitcoin’s block size. The fight was arcane. Essentially, Bitcoin Cash supporters thought the crypto should be primarily useful as a medium of exchange (in other words, you should be able to buy things with it), while the rest of the community wanted to prioritise the store of value function, or the ability to save it for future use.

Bitcoin SV—for “Satoshi Vision”—is even more controversial, given that it’s fronted by Craig Wright, an Australian computer scientist who dubiously claims to be Satoshi Nakamoto, the pseudonymous Bitcoin inventor. “I created Bitcoin,” he told Forbes in an interview in 2023. The UK’s High Court disagreed in March, ruling that the evidence is “overwhelming” that Wright did not write the initial Bitcoin whitepaper, is not Satoshi Nakamoto and did not create the “Bitcoin system”. Bitcoin SV was delisted by Coinbase in January but still maintains a market value of $1.6 billion.

Among blockchain zombies, Ethereum Classic (ETC) holds the unique distinction that it actually is the original Ethereum chain. What is widely known as Ethereum today is in reality a fork of ETC, created in 2016 to recover $60 million in stolen ether (worth $11.5 billion based on today’s prices). A significant minority of Ethereum backers worried about the moral hazard implications of altering the history of the ledger to recover funds, and they decided to continue maintaining ETC as the original and unaltered code base. One of the blockchain’s biggest backers is Connecticut firm Grayscale Investments, the world’s largest crypto asset manager, whose ex-billionaire founder, Barry Silbert, is an outspoken ETC bull. Ethereum Classic has a market value of $4.6 billion but generated fees of less than $41,000 in 2023.

Of the five spin-off blockchains Forbes analysed, none of the crypto industry insiders or data analysis firms we consulted could cite any serious uses for these platforms except for simply trading their tokens.

“What’s keeping these zombies alive is liquidity,” says one VC. “Litecoin was one of the first tokens that Coinbase supported back in the day. A lot of people owned litecoin.”

Adds Bob Summerwill, executive director at the Ethereum Classic Cooperative, “ETC is listed nearly everywhere because of its history, which turns into quite a lot of trading volume. Much of the activity is speculative.”

Riding ethereum’s coattails, ethereum classic tokens are trading 31 percent higher than they did a year ago, compared to a 77 percent gain for ether. Bitcoin Cash has outpaced bitcoin, which hit a record high in mid-March after a 121 percent surge in the last 12 months. Bitcoin Cash is up 164 percent over the same period.

The biggest group of zombies are would-be challengers to Ethereum. They mostly claim to be technological improvements on Vitalik Buterin’s 2014 creation, because Ethereum can process only a dozen transactions per second and is prone to sky-high fees during peak use. Tezos, founded later in 2014, was one of the first chains to incorporate a process known as proof-of-stake—as opposed to proof-of-work—to create new tokens. The details are bewildering (and vary by crypto project), but proof-of-stake is favoured by many crypto enthusiasts because it does not require the same electricity-wasting computing power as bitcoin mining.

Tezos raised $230 million in a 2017 initial coin offering (ICO), and the current market capitalisation for its XTZ token is $1.2 billion. However, it has been processing about 130,000 transactions daily, compared to 1.2 million for Ethereum, and it has just $66 million in so-called total value locked (TVL) in digital assets on its network. For blockchains like Ethereum, which are designed to host applications ranging from crypto exchanges to video games and NFTs, TVL is widely used as a measure of health. Ethereum, with more than 4,500 apps, has a TVL of $48 billion.

In terms of processing or “baker” fees, as Tezos refers to them, $5,640 was earned in February 2024 and $177,653 for all of 2023. Arthur Breitman, who founded Tezos with his wife, Kathleen, insists that dramatically understates the actual total. According to Breitman, 75 percent of the total fees paid to the network take the form of XTZ tokens which are typically taken out of circulation—or “burned”—and thus are not counted in its published revenue figures. Breitman estimates Tezos has $700 million in its treasury and maintains that only 20 percent of its funds are held in the XTZ token. “There’s a bunch of bitcoin, and then the rest is a diversified stock-and-bond portfolio,” he says.

That’s impossible to verify. The blockchain’s development is funded by a nonprofit called the Tezos Foundation, which is based in Switzerland. Its stated mission is the “promotion of the Tezos protocol through grants and other capital deployment vehicles”. In the first half of 2023, the Tezos Foundation awarded as much as $18 million to 31 new grantees. Grant recipients included a Philadelphia video game company building Tezos-compatible puzzles and a Singaporean talent agency specialising in digital art.

Then there is Algorand, which has a market cap of $2 billion and $500 million in its treasury. Once regarded as an “Ethereum killer” because of its reported ability to process 7,500 transactions per second, it brought in only $63,000 in blockchain transaction fees in 2023. “Their technology is probably right there with the other chains, but they’re not seeing much activity because they don’t have much community and talent beyond their founder [renowned Italian computer scientist and MIT professor Silvio Micali],” says one prominent crypto strategist.

Counters Eric Wragge, who runs business development for the Singapore-based Algorand Foundation: “We’re in that Uber mode—it lost money on every single person who got into a car.” They are also losing executives at a rapid clip. Over the last two years, the Algorand Foundation hired a new CEO and overhauled its entire C-suite.

Some blockchain zombies seem to trade solely based on the popularity of their creators. Cardano, another Ethereum competitor, was launched in 2017 after its co-founder, Charles Hoskinson, had a falling-out with Buterin, his Ethereum co-founder. Hoskinson’s blockchain is worth an astounding $23 billion with a TVL of $396 million. It brought in $3 million in fees last year, despite the Cardano Foundation itself saying it hasn’t yet moved out of its developmental stages.

Hoskinson himself seems to be the main attraction. He owns an 11,000-acre ranch in Wyoming, funds self-described alien hunters and recently opened an anti-aging and regenerative medicine centre in the town of Gillette. He is not always a reliable narrator. He claimed to have dropped out of a maths PhD programme at the University of Colorado, Boulder, but the school says Hoskinson was an undergrad who didn’t complete his degree. He has hinted for years about working for Darpa, the Pentagon’s prestigious research division. But he does reliably tout Cardano to his 980,000 followers on X.

Asks Bitwise’s Matt Hougan, “Is it a pre-revenue blockchain still building out its architecture, or is it just a future pilot that will never materialise?”

The 20 zombie blockchains called out on our table are just the largest examples of digital assets trading without any regard for the utility or viability of their underlying projects. There are many more roaming about. According to CoinGecko, more than 13,000 cryptocurrencies are listed on various exchanges, most having the characteristics of speculative penny stocks, except they don’t represent ownership in anything at all. Thanks to bitcoin’s surge, the total value of all crypto is around $2.5 trillion today.

Seems like an excellent shorting opportunity, but according to crypto trading firms, it’s difficult to bet against zombie blockchain tokens because it’s not easy to borrow significant amounts of the underlying tokens for short selling. Moreover, given crypto’s history of irrational and volatile trading, it’s extremely risky. Any token has the potential to transform into a memecoin based on nothing more substantial than a late-night tweet from Elon Musk.

Take the case of Ethereum Classic. In August 2020, when it was trading at around $6 per token, it faced three so-called 51 percent attacks in a single month. This occurs when a single token holder controls more than half of a network’s computing power, used to create blocks and therefore “govern” the platform. Had they been permanent (they were not), these “hostile takeovers” could have allowed the blockchain’s supposedly immutable ledger to be altered. In other words, anyone who owns 51 percent of a blockchain could mint unlimited tokens for himself. Despite being exposed as unsafe three times in a month, Ethereum Classic shrugged off its death blows in the summer of 2020 and today trades at $31.

The Department of Justice and the Securities and Exchange Commission’s approach to cracking down on crypto fraud and theft has been to go after large crypto exchanges—the enablers. FTX has been shuttered and its founder, Sam Bankman-Fried, is in jail. Binance’s founder, Changpeng Zhao, has been kicked out of the business, his exchange forced to pay $4.3 billion last year after he pleaded guilty to anti-money laundering and sanctions violations.

Two other large exchanges, Coinbase and Kraken, have each been sued by the SEC for acting as unregistered securities brokers and exchanges. Several zombie blockchain tokens, including cardano and algorand, were cited as being examples of securities in disguise.

Can token holders access the billions in capital being stored in the “treasuries” of the blockchain zombies? Unfortunately, it’s probably out of reach. “There would need to be a cause of action and actual harm from something like fraud,” says Yesha Yadav, associate dean at Vanderbilt University Law School, noting that past cases have been split on whether decentralised organisations or foundations can be held liable.

In September 2022, the feds sued the participants of a decentralised autonomous organisation called Ooki DAO, alleging that it was selling unregistered commodity futures. In June, a California court ordered the organisation to pay a fine of $644,000. That money is supposed to come out of its “decentralised” treasury, but the government is still awaiting payment. Two months later, a federal judge in New York dismissed a lawsuit filed against decentralised crypto exchange Uniswap, ruling that there was no centralised entity to serve as an “identifiable defendant”.

Don’t expect any of the cash-rich, do-nothing blockchains to shut down anytime soon. They are busy spending their money on long-shot projects. In March, the Stellar Development Foundation, the nonprofit presiding over zombie Stellar’s $2.5 billion treasury, announced it would invest $100 million in companies planning to use its new smart contract platform as it seeks to diversify beyond its mostly nonexistent payments business.

Buyer beware. The lunatics are running the crypto asylum.